In terms of the modern era of employment, traditional health insurance has been the cornerstone of employee benefits packages. Employers and employees alike have historically viewed these plans as a vital component of compensation, often equating the quality of a job offer with the extent and coverage of its health insurance benefits. However, this long-standing paradigm is facing increasing scrutiny as the adequacy and effectiveness of traditional health insurance in meeting modern healthcare needs are being called into question.

Insurance is failing your employees

Recent trends and data points are painting a concerning picture of employee sentiment toward these traditional health insurance plans. An indicator of this shifting sentiment is the significant drop in benefits satisfaction, which is now at a decade low, with only 61% of employees expressing satisfaction with their current benefits—a decline from the previous year as reported by MetLife. This decline is more than just a statistic—it’s a reflection of the growing frustration and financial strain employees experience under the weight of rising premiums, opaque policies, and inadequate coverage.

The Employee Benefit Research Institute (EBRI) adds another layer to this story, finding that only 55% of employees feel extremely or very satisfied with their health insurance plans. This stagnation in satisfaction levels, consistent over the past few years, reveals a critical disconnect between employee needs and the benefits provided by traditional insurance.

In this post, we will be taking a look at three critical ways that traditional health insurance may be failing your employees—and how health share membership might offer a more sustainable, flexible, and holistic solution to meet the needs of your team.

Failure #1: High costs and high premiums

The first, and likely most visible, shortcoming of traditional health insurance is the financial burden imposed by high costs and premiums. This isn’t just borne by your employees, though; as an employer, you too feel the weight of escalating premiums, which often make up a large chunk of your operating budget. This strain reaches wide, impacting budgets, savings, and overall financial wellbeing for all parties involved.

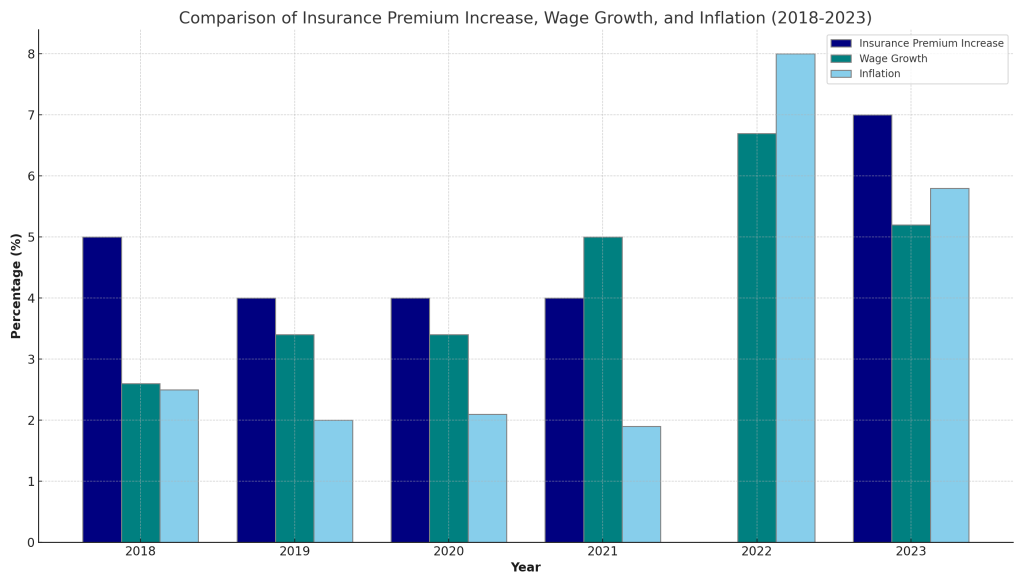

Over the years, the cost of health insurance premiums have only gone up. Some reports indicate that average costs for health plans rose by 6.4% in 2023, pushing the expenses to more than $13,800 per employee. This increase outpaces inflation and wage growth, so you can imagine the effect this is having on your team members. This is a barrier to financial stability and a source of constant worry to many.

Note that the KFF annual report in 2022 reported no increase in average insurance premiums, though the publication did acknowledge that its compiling methods that year may have contributed to minimizing an increase.

Failure #2: Complexity and lack of transparency

If you think about the way you have heard other people talk about their health insurance over the years, you’ve likely noticed the stories revolve around instances of confusion and frustration. The complex nature of insurance policies, with their near-endless terms, conditions, and caveats, often make it challenging for your employees to understand their coverage and entitlements fully.

Hidden Costs

One of the most criticized aspects of this issue is the prevalence of hidden costs. Beyond the apparent and predictable expenses like premiums and deductibles, there can be many indirect costs that are not immediately obvious, and that may need to be paid out of pocket. For example, the cost of a surgery might be covered, but further expenses related to the medical issue, like specialist fees or facility charges, may not be, leading to unexpected costs for the policyholder. A study by the American Medical Association indicated that 20% of medical claims are processed incorrectly, often resulting in people paying out of pocket for things they shouldn’t.

A survey by Bend Financial found that 56% of Americans do not understand their own health insurance plans, which often results in people either overpaying for unnecessary coverage or facing unexpected charges for supposedly covered services. This lack of clarity not only affects financial planning, but also impacts people’s healthcare decisions, as they might feel the need to forego necessary treatments due to the cost of uncertainties or the fear of dealing with the insurance bureaucracy.

Claims

The claims process itself is another area where opacity and complexity work to benefit only the health insurance companies. For many people, filing a claim is akin to stumbling through a dark maze of procedures, forms, and communications that seem to lead nowhere. One of the top consumer complaints regarding health insurance relates to delays in claims processing, denial of claims, and the frustrating back-and-forth often required to resolve their issues.

Failure #3: Limitations of provider networks

The third major shortcoming of traditional health insurance lies in the restricted choices and limited networks that dictate the terms of healthcare access for policyholders. These restrictions not only limit the choice of healthcare providers and specialists, but also introduce challenges and bureaucratic hurdles for people to jump through.

Traditional health insurance plans often come with a predefined network of healthcare providers. These networks are essentially lists of doctors, hospitals, and specialists that have contractual agreements with the insurance company to provide services at negotiated rates. While this arrangement can lead to lower costs for routine care, it doesn’t give the policyholder freedom to choose their preferred healthcare providers. If a policyholder’s trusted doctor or a recommended specialist is not part of their approved network, accessing services can result in substantially higher out-of-pocket costs or outright denial of coverage.

Seeking care from out-of-network providers is not only costlier, but also rigged with hoops to jump through. This can be particularly distressing when dealing with serious health conditions where timely and specialized care is critical. According to a report, out-of-network charges were nearly 300% higher than the Medicare rates for the same service, highlighting the financial predicament for patients looking for care outside of their insurance network.

Hurdles & Wait Times

Another way the complexity of health insurance manifests itself is in long waiting times for certain medical procedures and treatments. Prior authorization, a process where the insurance provider must approve a medical service before it is rendered, can lead to delays in receiving necessary care. A survey by the American Medical Association revealed that 64% of physicians reported waiting at least one business day for prior authorization decisions from insurers, with 30% reporting waiting at least three business days.

A growing answer to the failings of health insurance

If you find the current state of health insurance deflating, you’re not alone. We at Healthsharing Reviews think these major failings of insurance paint a picture of a system in urgent need of reform. It’s not likely to happen anytime soon, so we’d rather bring alternative solutions into focus, so you and your employees can enjoy stability and transparency and access to the healthcare that fits your needs. This is where health shares come in.

As an answer to the failings of insurance, health shares offer a community-based way to alleviate the financial burden of large medical expenses. These memberships are not just alternatives in terms of structure; rather, they represent a drastic shift in paradigm concerning how healthcare costs are approached, managed, and shared.

Let’s take a look at how health shares directly address the shortcomings of insurance:

- Affordability & Shared Responsibility: Health share memberships are known for their affordability, primarily stemming from their unique cost-sharing structure. Unlike traditional insurance premiums that keep increasing, health shares typically involve a more predictable and often lower monthly expense. These monthly payments are contributions to a communal fund, from which the medical expenses of the community are paid for. This collective structure leads to lower overall expenses for members, as the risks and costs are distributed across a larger group.

- Simplicity & Transparency: One of the most appealing aspects of health shares is their straightforward structure. These programs generally have clear guidelines on member responsibilities and the sharing process, making it easier for members to understand what is expected of them and what they can expect in return.

- Freedom in Healthcare Providers: Unlike traditional health insurance plans that restrict members to specific networks, health shares usually offer greater flexibility in choosing healthcare providers and specialists. This puts you in charge of your own healthcare, so you can find the best care possible and you can and rest assured that your health share will not reject the provider.

Health shares are growing fast, and for many they are a compelling answer to the major failings of traditional health insurance. By offering affordability, simplicity, and flexibility, health shares can benefit your employees where insurance has failed them.